Risk Exposure

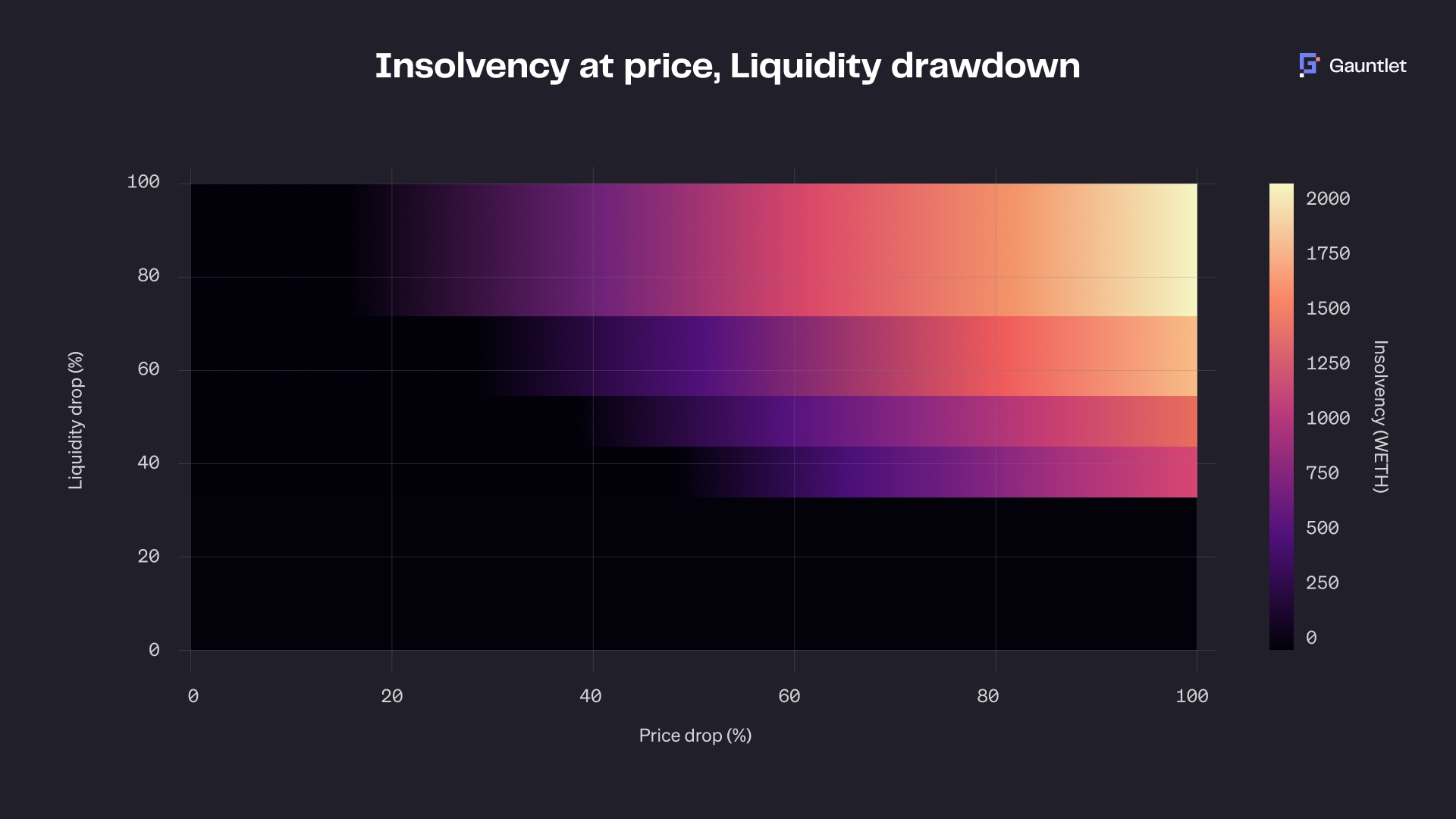

The primary risk in lending markets stems from insolvent debt, which occurs when risky positions (health factor < 1) aren't liquidated promptly. This typically happens during market stress, when collateral prices fall sharply, and insufficient onchain liquidity makes liquidations unprofitable. Since liquidators operate on profit incentives, they won't act on underwater positions if market conditions make liquidation unprofitable.

Our market exposure strategy quantifies potential insolvent debt under severe market conditions. We analyze two key metrics:

Price risk: Maximum expected daily price decline

Liquidity risk: Maximum expected daily DEX liquidity reduction

If a market's exposure under an X% drop in the collateral asset price exceeds the liquidity available during a Y% liquidity crunch, we take action to decrease our exposure. We determine X and Y based on historical data, typically setting:

X = the 99th percentile day-over-day price drop

Y = the 99th percentile day-over-day drop in DEX liquidity over the past year

We reduce our position if a market's potential exposure under these stress conditions exceeds available liquidation capacity. This conservative approach applied to Gauntlet Prime and Core Vaults, can maintain near-zero insolvency risk for our vaults, targeting insolvent debt below 10 basis points of total vault TVL even in extreme scenarios.

We continuously simulate the expected number of liquidations and the net volume over adverse price and liquidity scenarios. As described above, when expected insolvencies under the prescribed liquidity and price drawdown conditions exceed our tolerance thresholds, we reduce our vault’s exposure to the at-risk markets as much as possible. This entails reallocating liquidity from markets that are more likely to experience insolvency to a safer market early and often. We will reallocate supply to the idle market if no suitable lending markets exist.

We actively monitor leveraged positions on other prominent DeFi protocols such as Aave, Compound, Spark, and Gearbox. Significant liquidations on these protocols can rapidly deplete the liquidity available for liquidations on Morpho. By monitoring the risk profiles of these protocols, we can anticipate and preemptively adjust our vault’s exposure to markets with bad debt risk.

Was this helpful?